“I have $40,000 saved, but properties in my area are around $700,000. Do I really need to wait another three years to save up $140,000?”

This is one of the most common questions I hear from first home buyers. The traditional advice has always been “save 20% to avoid Lenders Mortgage Insurance,” but the reality is more nuanced. For many buyers, waiting years to save means watching property prices increase faster than they can save, effectively pushing homeownership further away.

The good news? Buying with a smaller deposit can be a strategic decision when done correctly.

Understanding Lenders Mortgage Insurance (LMI)

LMI is a one-off premium added to your loan when you borrow more than 80% of a property’s value. Here’s what you need to know: it protects the lender, not you. If you default and the property sells for less than you owe, the insurer covers the lender’s loss.

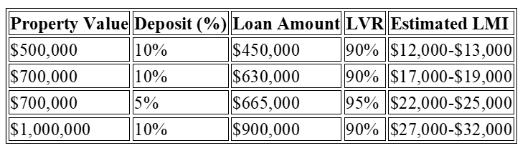

How Much Does LMI Cost?

LMI ranges from 1% to 5% of your loan amount. Here are real examples:

LMI Ranges

Key Insight: Increasing your deposit from 5% to 10% can save $5,000-$8,000 in LMI on a typical property.

Six Ways to Avoid Paying LMI

- First Home Guarantee (Most Popular)

The government guarantees part of your loan, eliminating LMI entirely. Buy with just 5% deposit and save $15,000-$40,000+ depending on property value.

Requirements: Must use participating lender, property price caps apply, limited places available annually.

- Professional Occupation LMI Waivers

Certain professions get special treatment:

- Medical professionals: Often 90-95% LVR without LMI

- Legal professionals: Typically, 90% LVR

- Accountants: Usually, 90% LVR

Real Example: Dr. James purchased an $850,000 property with 10% deposit. His LMI would have been $28,000-$32,000, but his lender waived it entirely.

- Guarantor Loans (Family Pledge)

A family member uses equity in their property as security, eliminating LMI. They don’t give you money; they offer their property as additional security for typically 10-20% of your loan.

- Save a Full 20% Deposit

The traditional approach still works but consider the opportunity cost. If properties are rising 6% annually and you need 18 months to save an extra $70,000, that property will increase by approximately $63,000 in value while you save.

- First Home Super Saver Scheme

Release up to $50,000 from your super to boost your deposit, potentially reaching 15-20% without needing to wait years.

- Shared Equity Schemes

Some state governments take an equity stake in your property, reducing your loan amount below 80% and avoiding LMI.

Should You Pay LMI or Wait?

Pay LMI When:

The math works in your favor. Calculate: Expected price growth vs LMI cost.

Example:

- Property: $700,000, growing at 6% annually

- Time to save additional 10%: 18 months

- Expected price increase: $63,000

- LMI cost at 10% deposit: $17,000

- Verdict: Pay LMI now. Waiting costs $63,000 to save $17,000.

Your finances are strong: You can comfortably afford repayments, have emergency savings, and stable income.

Rent is high: At $600/week, you’re paying $31,200 annually in rent—money that could build equity instead.

Wait and Save More When:

- Repayments would stretch your budget uncomfortably

- You don’t have emergency savings beyond deposit

- Property prices are flat or declining

- You can reach 20% within 6-8 months

Common LMI Misconceptions

Myth 1: “LMI is wasted money” Not when property prices are rising faster than you can save. It can be a strategic investment.

Myth 2: “I can get LMI refunded if I refinance” No. LMI is non-refundable and non-transferable. Refinance above 80% LVR means paying LMI again.

Myth 3: “LMI protects me if I can’t make repayments” No. LMI protects the lender only.

Myth 4: “All lenders charge the same LMI” LMI costs vary significantly between lenders—always compare.

Real Case Study: When LMI Made Sense

Emma, a Sydney teacher with $60,000 saved (9% deposit), wanted a $650,000 townhouse.

Her Options:

- Buy now with LMI: Pay $21,000 LMI, lock in $650,000 price

- Wait 24 months: Property grows to $716,000, pay $56,000 in rent

The Decision: Emma bought with LMI. She avoided $66,000 in price growth and saved $56,000 in rent. Net benefit: approximately $101,000 ($66,000+$56,000-$21,000) over waiting.

Your Action Plan

- Calculate your LVR and get accurate LMI quotes from multiple lenders

- Check eligibility for First Home Guarantee, professional waivers, or guarantor options

- Run the numbers: Compare LMI cost vs expected price growth vs rent costs

- Choose the right lender: LMI pricing and policies vary significantly

Key Takeaway

Low deposit loans aren’t about buying before you’re ready—they’re a strategic tool when:

- You can genuinely afford the repayments

- Property market conditions favor buying now

- The cost of waiting exceeds the cost of LMI

- You have options to avoid or minimize LMI

There’s no universal right answer. What matters is making an informed decision based on your specific circumstances and market conditions.

Are you considering buying with less than 20% deposit? What’s your biggest concern—LMI cost, market timing, or serviceability? Share in the comments.

Chirag specialise in helping first home buyers and investors to access low deposit loans, professional LMI waivers, and the First Home Guarantee scheme. We compare LMI costs across lenders to ensure you get the best outcome.

📞 Ready to explore your options? Book a free consultation at nextgenjc.com.au or call 0478797785