“I’ve been saving for three years, but I still don’t know if I’m ready to buy.”

I hear this from first home buyers almost every week. They’ve done the hard part—built up savings, researched suburbs, scrolled through countless property listings—but they’re stuck at the starting line because they don’t have a clear roadmap.

The path to homeownership isn’t just about having enough money in the bank. It’s about understanding the process, knowing your true borrowing capacity, timing your entry into the market, and avoiding the costly mistakes that can delay your purchase by months or even years.

Let me walk you through the complete roadmap that will take you from dreaming about your first home to holding the keys.

Step 1: Understand Your True Borrowing Capacity (Not Just What Online Calculators Tell You)

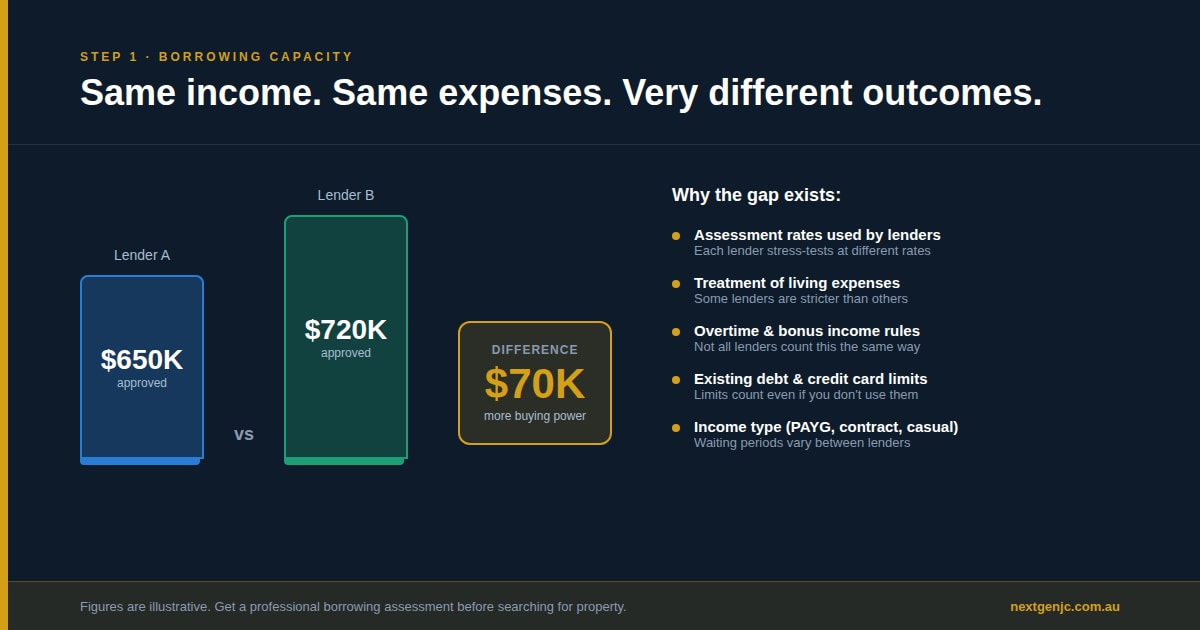

Most first home buyers start with an online borrowing calculator. They plug in their income and expenses, see a number, and either get excited or discouraged. But here’s what those calculators don’t tell you:

Your borrowing capacity isn’t fixed—it varies significantly between lenders. One lender might approve you for $650,000 while another offers $720,000 for the exact same income and expenses. Why? Because each lender has different:

- Assessment rates (the interest rate they use to test if you can afford repayments)

- Treatment of living expenses

- Rules about PAYG (salary), overtime, bonuses, and rental income

- Policies on existing debts and credit cards

Your profession matters. If you’re a doctor, allied health professional, lawyer, accountant, or other professional, some lenders will offer you higher loan-to-value ratios and waive lenders mortgage insurance, dramatically increasing your borrowing capacity.

Timing matters. If you’ve recently changed jobs, gone casual or contract, or taken parental leave, different lenders have different waiting periods. Knowing which lender to approach can be the difference between getting approved now or waiting another six months.

Before you start looking at properties seriously, get a professional assessment of your borrowing capacity. Not a bank’s generic pre-qualification, but a strategic analysis that identifies which lenders will give you the strongest position.

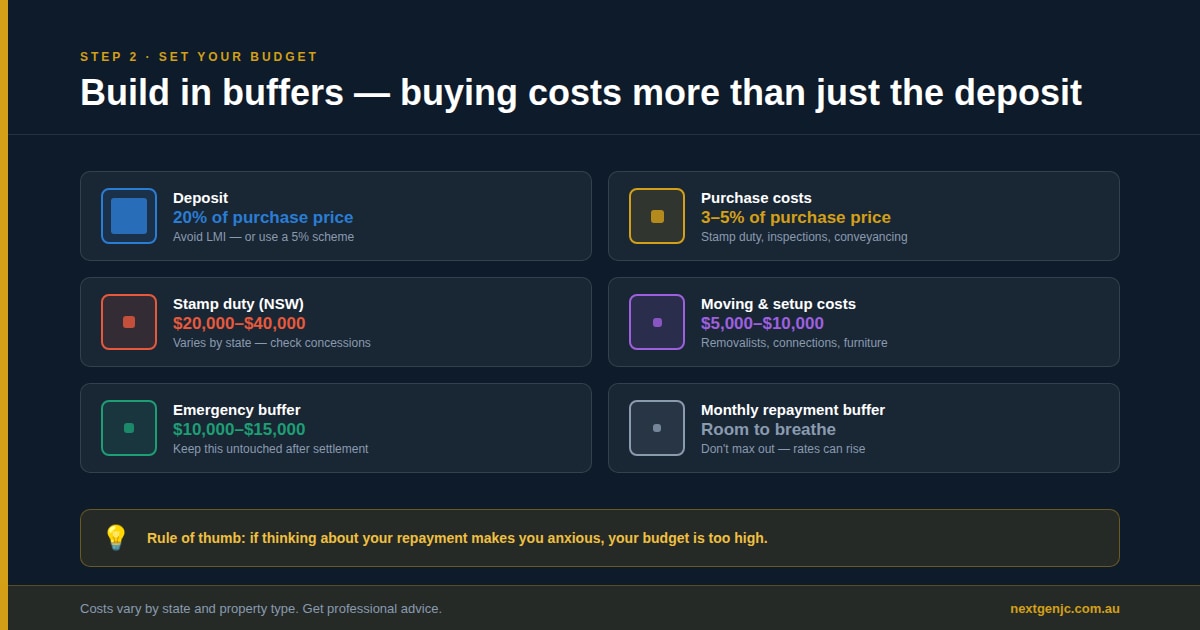

Step 2: Set Your Realistic Budget (And Build in Buffers)

Once you know your borrowing capacity, resist the temptation to borrow the maximum amount.

Your budget should account for:

- Deposit: Ideally 20% to avoid LMI, but there are legitimate strategies for buying with 5-10% (more on this in Article 3)

- Purchase costs: Stamp duty, transfer fees, building and pest inspections, conveyancing fees—typically add 3-5% to your purchase price

- Moving and setup costs: Often overlooked but can easily reach $5,000-10,000 for removalists, connection fees, initial furniture and appliances

- Emergency buffer: Keep at least $10,000-15,000 in savings after settlement for unexpected repairs or expenses

- Monthly repayment comfort zone: Just because you can afford $3,500/month doesn’t mean you should stretch to that limit. Consider potential interest rate increases, life changes, and your lifestyle preferences.

A good rule of thumb: if your ideal repayment amount is making you anxious when you think about it, your budget is too high.

Step 3: Get Your Finances in Order (6-12 Months Before Buying)

Lenders scrutinise your last 3-6 months of bank statements. Everything matters.

Start preparing early:

- Boost your savings pattern: Show consistent savings, even if small amounts. Regular $500-1,000 monthly transfers into a separate savings account demonstrate financial discipline.

- Clean up your spending: Minimise Afterpay, zip pay, and buy-now-pay-later services. Reduce or close unused credit cards—even if you don’t use them, lenders count their limits as potential debt. Cut down on gambling transactions (even small sports betting) and explain large deposits that aren’t from your salary.

- Stabilise your employment: Avoid job changes within 6 months of applying if possible. If you must change jobs, stay in the same industry at a similar or higher salary level.

- Check your credit score: Download your free credit report from Equifax. Dispute any errors and understand what’s on there. Don’t make multiple loan applications in a short period—each inquiry impacts your score.

- Document everything: Start collecting payslips, tax returns, bank statements, and proof of savings origin. Lenders want to see that your deposit is genuine savings, not a last-minute loan from family (unless structured correctly as a gift).

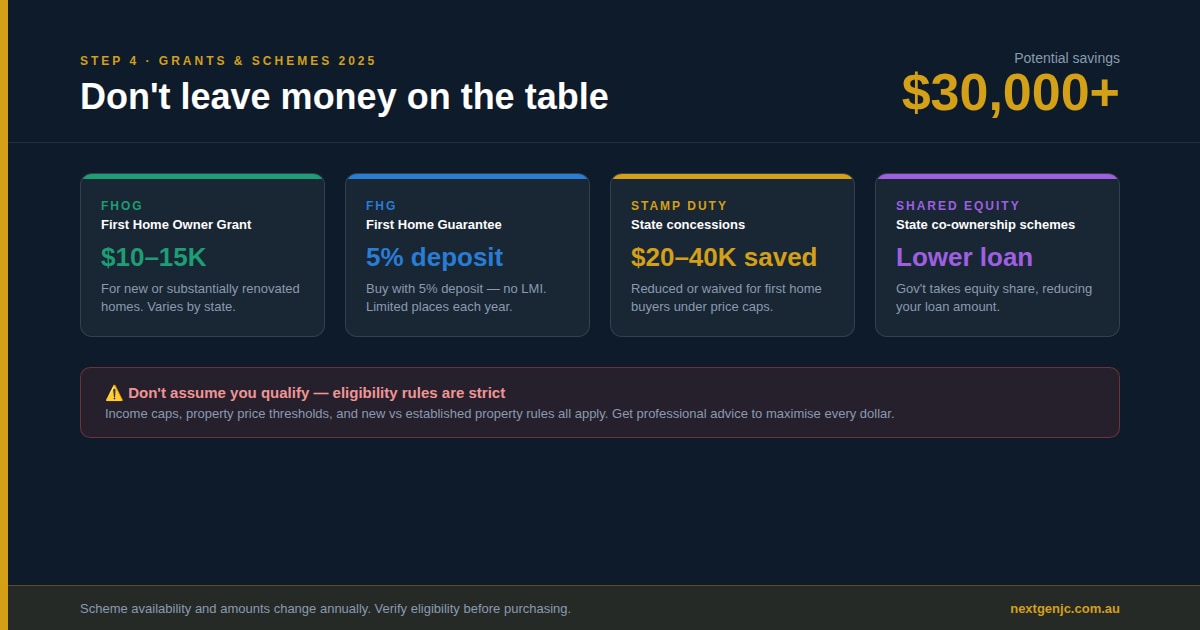

Step 4: Understand Government Grants and Schemes (This Can Save You $30,000+)

This is where many first home buyers leave money on the table.

The grants and schemes available in 2025 can dramatically reduce your upfront costs:

- First Home Owner Grant (FHOG): Varies by state, typically $10,000-15,000 for new or substantially renovated homes. Each state has different eligibility criteria and property price caps.

- First Home Guarantee (FHG): Federal government scheme that allows you to buy with just 5% deposit without paying LMI. Limited places available each year—applications are competitive.

- Regional First Home Guarantee: Similar to FHG but for regional areas, with more generous allocations.

- Stamp duty concessions: Every state offers either reduced or waived stamp duty for first home buyers under certain price thresholds. In NSW, this can save you $20,000-40,000.

- Shared Equity Schemes: Some states offer schemes where the government takes an equity share in your property, reducing your loan amount.

The catch? These schemes have specific eligibility requirements around income thresholds, property prices, and whether you’re buying new or established properties. You need to know which schemes you qualify for before you start looking at properties.

We’ll dive deeper into each of these in Article 2, but the key message is: don’t assume you know what you’re eligible for. Get professional advice to maximise every available benefit.

Step 5: Get Pre-Approved (Not Just Pre-Qualified)

There’s a critical difference:

- Pre-qualification: A quick assessment based on information you provide. Not verified. Not guaranteed. Worth very little when making an offer.

- Pre-approval: Full application with income verification, credit check, and conditional approval from a lender. Valid for 3-6 months. Shows sellers you’re a serious buyer.

A proper pre-approval gives you:

- Confidence in your budget when inspecting properties

- Credibility with real estate agents who will prioritise you

- Negotiating power when making offers

- Faster settlement because most documentation is complete

But here’s what most people don’t realise: getting pre-approved with the wrong lender can actually work against you. If you get pre-approved with a lender that’s difficult to deal with, slow to settle, or has restrictive policies, you might lose out on properties even with pre-approval in hand.

Work with a broker who knows which lenders offer the best combination of approval strength, competitive rates, and efficient settlement processes.

Step 6: Start Your Property Search (With Strategy, Not Just Emotion)

Now you’re ready to seriously look at properties. But approach this strategically:

- Define your non-negotiables: Location, property type, bedrooms, parking. Know what you can compromise on and what you can’t.

- Understand market conditions: Are you in a buyer’s market or seller’s market? This changes your negotiation approach and how quickly you need to move.

- Look beyond the pretty photos: Focus on structural quality, location fundamentals, and future growth potential. A renovated apartment might look Instagram-worthy, but a unrenovated house in a better suburb often delivers better long-term value.

- Get building and pest inspections: Never skip this, even for newer properties. A $500 inspection can save you from a $50,000 mistake.

- Consider future resale: Even though it’s your first home, think about who would buy it from you in 5-10 years. Properties with broad appeal hold their value better.

Step 7: Make Your Offer and Navigate to Settlement

Once you find the right property:

- Don’t overpay because of emotion: Set your maximum price before the auction or negotiation and stick to it. There will always be another property.

- Get your conveyancer involved early: They’ll review the contract, identify any issues, and guide you through the legal process.

- Activate your pre-approval: Contact your broker immediately to confirm the property meets your lender’s criteria and start final approval.

- Stay responsive: Settlement typically takes 30-60 days. Respond quickly to any lender requests for additional information.

Final checks before settlement: Do a final inspection, arrange insurance, and organise utilities connection.

Common Timeline: How Long Does It Really Take?

Here’s a realistic timeline for most first home buyers:

Months 1-3: Build savings, clean up finances, improve credit score

Months 4-6: Get professional borrowing assessment, understand grant eligibility, organise documentation

Month 6-7: Submit full pre-approval application, receive conditional approval

Months 7-10: Active property search, inspections, making offers

Months 10-11: Offer accepted, exchange contracts, final loan approval

Month 12: Settlement and move in

Total timeline: 12-18 months from starting to plan seriously to holding keys

Can it be faster? Absolutely. If your finances are already in great shape and you’re pre-approved, you could be in your home within 3-6 months. But for most first home buyers, giving yourself 12+ months removes stress and allows you to make better decisions.

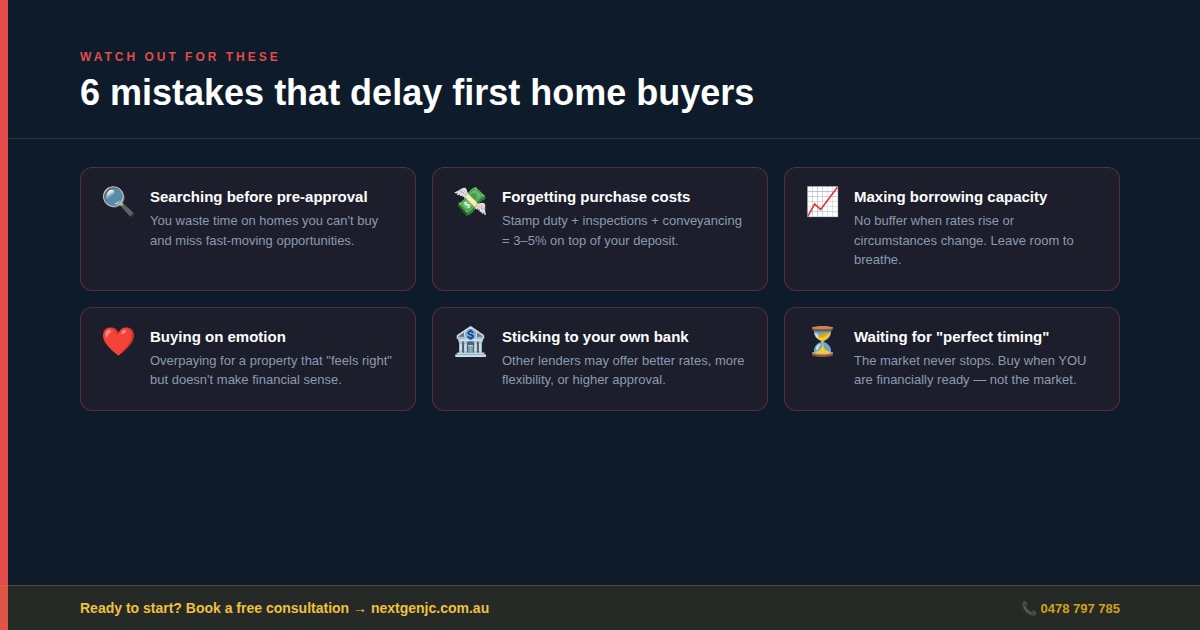

The Biggest Mistakes That Delay First Home Buyers

After working with multiple first home buyers, I see the same mistakes repeatedly:

- Starting the property search before getting pre-approved: You waste time looking at properties you can’t afford or miss opportunities because you can’t move quickly.

- Not accounting for all purchase costs: They have deposit saved but forget about stamp duty, inspections, and conveyancing, then scramble to find additional funds.

- Maximising their borrowing capacity: They borrow the absolute maximum, then struggle with repayments when interest rates increase or life circumstances change.

- Choosing properties based purely on emotion: Falling in love with a property that doesn’t make financial sense or suit their actual lifestyle needs.

- Not shopping around for lenders: They go straight to their existing bank without realising other lenders offer better rates, features, or lending criteria.

- Waiting for the “perfect time”: The market is always doing something—rising, falling, stabilising. If you wait for perfect conditions, you’ll wait forever. The best time to buy is when you’re financially ready and find the right property.

Your Action Plan This Week

If you’re serious about buying your first home, here’s what to do in the next 7 days:

- Download your credit report and review it for errors or issues, its free.

- Calculate your current savings rate and identify where you can increase it

- Review your last 3 months of bank statements through a lender’s eyes—what would concern them?

- Research suburbs that match your budget and lifestyle needs

- Book a consultation to get your borrowing capacity professionally assessed and understand which grants you qualify for

The journey to your first home is exciting, but it requires planning, patience, and the right professional guidance. You don’t have to navigate this alone.

What’s Next in This Series

In Article 3, we’ll dive deep into government grants and schemes available in 2025, showing you exactly how to maximise every dollar of support available to first home buyers.

What’s your biggest concern or question about buying your first home? Are you worried about saving enough deposit? Confused about borrowing capacity? Unsure about timing? Drop your questions in the comments—I read and respond to every one.

Chirag is a, mortgage broking specialists serving first homebuyers, investors, SMSF trustees, and professionals across Australia. We are here to provide solutions on the principle that everyone deserves personalised advice based on unique individual circumstances, not generic solutions.

Ready to start your first home journey? Book a free consultation at nextgenjc.com.au or call 0478797785, email – teamnextgenjc@gmail.com

Ready to start your first home journey? Book a free consultation at nextgenjc.com.au or call 0478797785, email – teamnextgenjc@gmail.com

Download First Home Buyer Checklist