Last month, I met a couple who had been saving for their first home for four years. With $60,000 saved, they were looking at apartments in Sydney’s outer suburbs around the $550,000 mark.

After reviewing their situation, I showed them how they could comfortably afford a $700,000 property in a better location. The difference? Understanding how to combine government grants and schemes. Through stamp duty savings, using the First Home Guarantee to eliminate LMI, and strategically structuring their application, they accessed more than $45,000 in support—benefits they didn’t even know existed.

This is extremely common. Around one-third of first home buyers used a federal guarantee scheme last financial year, yet many others miss out simply because they don’t know what’s available or how to apply.

In this guide, I break down every major federal and state scheme available in 2025, so you don’t leave money on the table.

Federal Government Schemes (Available Australia-Wide)

1. First Home Guarantee (FHG)

The Game Changer for 5% Deposit Purchases

The First Home Guarantee allows first home buyers to purchase with as little as 5% deposit without paying Lenders Mortgage Insurance (LMI).

How It Works

The government guarantees up to 15% of the property price, allowing you to avoid LMI—often $10,000–$20,000 for a typical first home purchase.

2025 Updates

- From 1 October 2025, income caps will be removed.

- The Regional First Home Buyer Guarantee will be discontinued, with support absorbed into the expanded national scheme.

Eligibility

- No property ownership in the last 10 years

- Australian citizen or permanent resident

- Must live in the property

- Must use a participating lender

- Property must be under the price caps (varies by region): NSW metro: $1.5M, NSW other: $800k VIC metro/regional centres: $950k, other VIC: $650k Other states: generally $600k–$900k

Real Example

On a $600,000 purchase with 5% deposit ($30,000), LMI would usually cost $15,000–$17,000. Under the FHG, this cost is completely removed.

Tip:

The scheme doesn’t ease serviceability assessment—it simply removes LMI.

2. First Home Super Saver Scheme (FHSSS)

Use your superannuation to save for a deposit at a lower tax rate.

How It Works

You make voluntary contributions to your super (before or after tax). These grow tax-effectively, and you can withdraw them + earnings to use as your deposit.

Key Details

- Up to $50,000 can be released (increased from $30,000)

- Up to $15,000 per year

- Both concessional and non-concessional contributions count

- Must apply through the ATO before signing a contract

Example

If you earn $85,000 and salary sacrifice $15,000 into super each year for two years, you could save $3,500–$4,000 in tax compared with saving outside super.

Strategy Tip: Start early—this works best if you’re 1–3 years away from buying.

3. Help to Buy (Shared Equity Scheme)

The government contributes up to:

- 40% for new homes

- 30% for existing homes

You then own the property jointly, with no rent or interest paid on the government’s share.

Key Points

- Reduces loan size and repayments

- Government shares in capital gain or loss

- You can buy back the government’s share anytime

- Income limits apply

- Property price caps apply

As of late 2025, commencement is not yet confirmed. Check with your broker.

As of late 2025, commencement is not yet confirmed. Check with your broker.

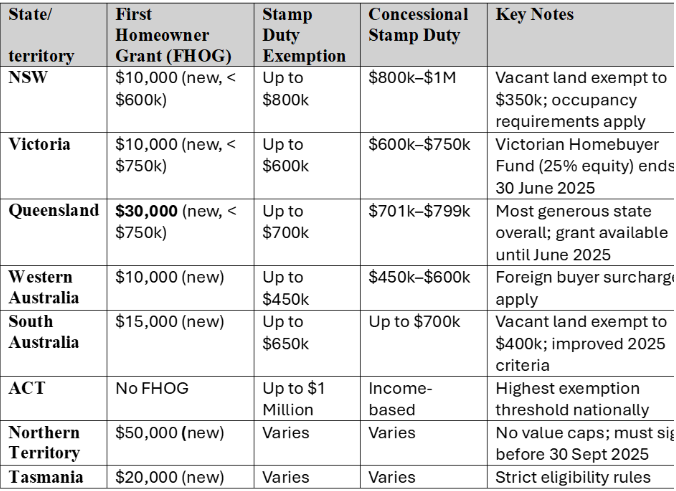

State-by-State First Home Buyer Benefits Comparison

Here’s a complete breakdown of what each state and territory offers first home buyers in 2025:

Note – Please check the state website for the latest update as there can be a change in the scheme.

Powerful Combinations: Where You Get the Most Support

Queensland – New Home Under $700k

Queensland – New Home Under $700k

· $30,000 FHOG

· $24,000 stamp duty exemption

· $17,000 LMI savings via FHG = $71,000 support

NSW – Established Home Under $800k

NSW – Established Home Under $800k

· $31,000 stamp duty exemption

· $15,000 LMI savings = $46,000 support

Victoria – New Home Under $600k

Victoria – New Home Under $600k

· $10,000 FHOG

· $31,000 duty exemption =$41,000 support

Common Mistakes That Cost Buyers Tens of Thousands 1. Not applying on time – Some benefits cannot be claimed after settlement. 2. Choosing established when new unlocks far more benefits – New homes often access $10k–$50k in grants. 3. Going slightly over price caps – An $805k NSW property could cost $31k more than one at $795k. 4. Using a non-participating lender – If your lender is not part of the Home Guarantee Scheme, you miss out entirely. 5. Missing occupancy requirements – Failing to move in or stay long enough can trigger repayments + penalties.

1. Not applying on time – Some benefits cannot be claimed after settlement. 2. Choosing established when new unlocks far more benefits – New homes often access $10k–$50k in grants. 3. Going slightly over price caps – An $805k NSW property could cost $31k more than one at $795k. 4. Using a non-participating lender – If your lender is not part of the Home Guarantee Scheme, you miss out entirely. 5. Missing occupancy requirements – Failing to move in or stay long enough can trigger repayments + penalties.

Your Action Plan:

How to Access These Benefits

Step 1: Confirm eligibility

Check residency, first home status, and timeline.

Step 2: Calculate total support available

Add up grants, stamp duty savings, and LMI savings.

Step 3: Choose a participating lender

Your broker should manage this.

Step 4: Gather your documents

ID

Citizenship/PR proof

Statutory declarations

Contract of sale

Step 5: Apply at the correct time

FHG → via lender

Stamp duty → via conveyancer

FHOG → via lender or state revenue office

FHSSS → via ATO

Step 6: Meet residence requirements

Move in and stay for the required period.

Frequently Asked Questions

Can I use the First Home Guarantee and FHOG together?

Yes—they complement each other.

What if I owned property before 2015?

You may still qualify for federal schemes (10-year rule).

Do these schemes apply to apartments?

Yes, except where grants require new builds.

Can I use these for an investment property?

No—all require owner-occupation.

What if I need to move for work?

Hardship exemptions may apply.

Why Professional Guidance Matters

I regularly meet buyers who lose $20,000–$40,000 because they applied incorrectly, missed deadlines, or didn’t structure their loan strategically.

A good mortgage broker doesn’t just find a competitive rate—they help you unlock every dollar of support.

What’s Next in This Series

“Low Deposit Home Loans: What You Need to Know”

Need Help?

If you’re unsure which schemes you qualify for or how to combine them: Book a free consultation: nextgenjc.com.au

Book a free consultation: nextgenjc.com.au  Call: 0478 797 785

Call: 0478 797 785  Ask your question in the comments—I’m here to help.

Ask your question in the comments—I’m here to help.

Chirag at Next Gen JC helps first home buyers across Australia maximise available grant and scheme.